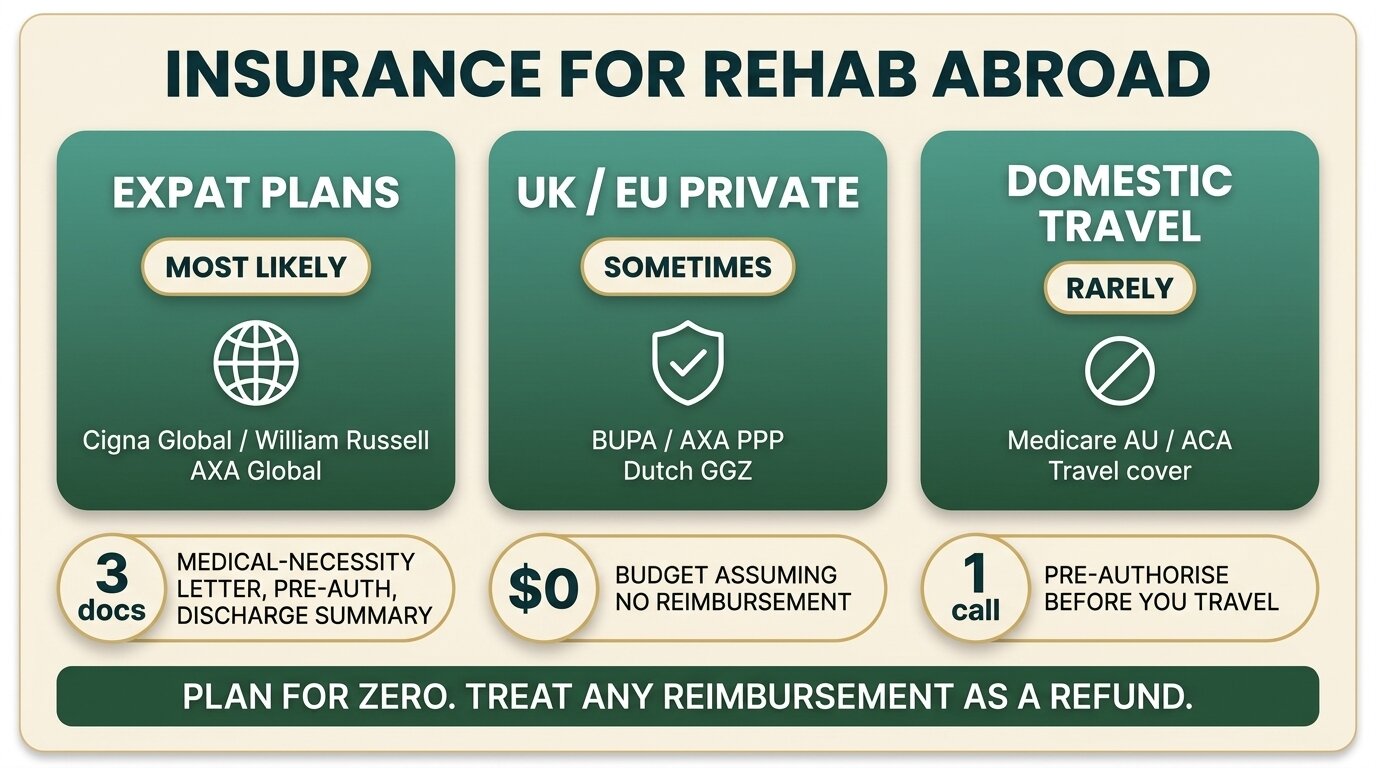

Key Takeaways

- Sometimes yes, sometimes no — and you usually have to fight for it. Expat international plans (Cigna Global, William Russell) are the most likely to pay; domestic plans (Australian Medicare, UK NHS, US ACA marketplace) generally won’t.

- UK private medical (BUPA, AXA PPP, Aviva, Vitality) sometimes covers UK-based addiction treatment with strict day caps, but covering an overseas residential stay is rare and usually requires explicit pre-authorisation.

- Dutch zorgverzekering can reimburse GGZ addiction care under tight conditions — referral letter, contracted provider, and prior approval — and overseas approval is the exception, not the rule.

- One Step Rehab is private-pay. We do not direct-bill insurers, but we provide the full documentation pack (admission letter, clinical formulation, weekly notes, discharge summary, itemised invoice) so you can submit a reimbursement claim.

- Plan your budget assuming zero reimbursement. If a claim succeeds, treat it as a refund — not the funding model.

Sometimes yes, sometimes no, and you usually have to fight for it. A small number of clients we admit each year do recover part of their fee from an insurer. Most pay up front and treat any reimbursement as a bonus. Coverage depends on three things: the type of policy you hold, the wording around overseas and out-of-network care, and how clean your medical-necessity documentation is. Despite parity laws like the US Mental Health Parity and Addiction Equity Act of 2008, residential substance use treatment remains one of the most restricted benefits in private insurance globally (Dickson-Gomez et al., Drug Alcohol Depend Rep, 2022).

Which Types of Insurance Actually Cover Inpatient Rehab Abroad?

The short list of policies that sometimes pay for overseas residential rehab: international expat plans (Cigna Global, William Russell, AXA Global Healthcare), some UK private medical policies with specific addiction riders, certain Dutch zorgverzekering pathways, and US PPO out-of-network benefits. Domestic Australian, Irish, and ACA marketplace plans almost never cover treatment outside their home country.

The rough hierarchy, from most likely to pay to least likely:

| Policy type | Likelihood of coverage | Main catch |

|---|---|---|

| Expat international plans (Cigna Global, William Russell, AXA Global) | Moderate — best of the lot | Addiction is often an add-on or higher tier only |

| UK private medical (BUPA, AXA PPP, Aviva, Vitality) | Low for overseas, moderate for UK clinics | Annual day caps; overseas requires explicit approval |

| Dutch zorgverzekering (basisverzekering + aanvullend) | Low to moderate, with a GP referral | Reimbursement only via specific GGZ pathway |

| US PPO out-of-network (Aetna, Cigna US, BCBS, UHC) | Low — partial reimbursement only | High deductible; usually pays a percentage of “allowed amount”, not your bill |

| Australian private hospital cover (Medibank, Bupa AU, HCF) | Very low | Generally only registered Australian private hospitals |

| US ACA marketplace (HMO/EPO) | Near zero | Network is geographically restricted |

| Travel insurance | Near zero | Pre-existing conditions and “elective” treatment are excluded |

How Does UK Private Medical Insurance Handle Overseas Rehab?

UK private medical insurers will sometimes pay for residential addiction treatment, but the day allowance is tightly capped — Bupa publicly references 28, 45, or 90 days depending on the policy, and only covers one course of addiction treatment per member lifetime in most plans (Bupa UK, 2026). Overseas treatment is rarely pre-approved.

BUPA, AXA PPP Healthcare, Aviva, and Vitality all sell mental-health-inclusive policies in the UK, but addiction is treated as a special case — often a rider, often excluded entirely from “core” mental health benefits, and almost always restricted to a specific list of contracted UK clinics. To get an overseas stay paid for, you usually need:

- A written referral from your GP or treating psychiatrist documenting medical necessity

- Pre-authorisation in writing before you travel — not a claim after the fact

- A clinical case that the UK contracted facilities can’t meet your needs (rare for addiction)

- An accepted private hospital code, which most overseas residential rehabs (including us) don’t hold

If you already have a BUPA or AXA policy with mental-health cover, call the medical claims line before you book anything. Get a reference number for the conversation. Ask for the decision in writing.

Can the Dutch Zorgverzekering Pay for Rehab Abroad?

The Dutch basisverzekering legally covers GGZ specialist mental health and addiction care, and reimbursement for overseas treatment is possible in narrow circumstances — usually requiring a GP referral, a treatment plan accepted by the insurer, and prior written approval. Reimbursement rates depend on whether your provider is contracted (gecontracteerd) or not (CZ Zorgverzekering, 2026).

Practically, Dutch clients we admit either:

- Pay up front, submit an itemised invoice and clinical documentation through their insurer’s nota indienen portal, and recover a fraction back under the non-contracted (“ongecontracteerde zorg”) rate — typically 50% to 80% of the Nederlandse Zorgautoriteit (NZa) maximum tariff

- Use a restitutiepolis (the more flexible policy type that pays out-of-contract providers at a higher rate) — these are less common but pay better for non-Dutch clinics

- Use private savings or family funding and write the trip off as out-of-pocket

If you have a Dutch huisarts (GP) you trust, ask for a verwijsbrief (referral letter) stating that residential treatment is medically necessary and explaining why a Dutch GGZ inpatient bed isn’t workable. That single document does more for a reimbursement claim than anything else.

Will Australian Medicare or Private Health Cover Overseas Rehab?

Almost never. Medicare excludes overseas treatment except in tightly defined reciprocal-care emergencies, and Australian private hospital cover (Medibank, Bupa AU, HCF, NIB) is restricted to registered Australian private hospitals. Most Australian clients who come to One Step fund the stay privately, sometimes through early-release superannuation on compassionate grounds.

Medicare in Australia covers GP appointments, addiction medicine specialist consultations, public hospital detox, and up to 10 psychology sessions per year under a Mental Health Care Plan — none of which travels with you to Thailand. Private hospital cover may partially offset stays in Australian private rehab facilities, but standalone residential rehab abroad falls outside the standard hospital networks that insurers contract with.

The route most Australians use to fund overseas treatment is the Australian Taxation Office’s early-release-of-super provision on compassionate grounds — for medical treatment not available in the public system, or where the wait time makes it medically unreasonable. We’ve covered this in detail in our guide to accessing superannuation for overseas treatment.

How Do US Insurance Plans Treat Inpatient Rehab Outside the US?

The Mental Health Parity and Addiction Equity Act of 2008 (MHPAEA) requires US group health plans to treat substance use benefits no more restrictively than medical benefits, but parity applies within the plan’s network and benefits — it does not force any plan to cover overseas providers (CMS, 2025). ACA marketplace HMO/EPO plans almost never pay for treatment abroad. PPO plans sometimes pay a small percentage of an “allowed amount” as out-of-network reimbursement.

What we’ve seen with US clients:

- HMO and EPO plans: Closed network. Overseas treatment is not a covered benefit. No reimbursement, full stop.

- PPO plans (Aetna, Cigna US, BCBS, UHC): Out-of-network benefits may apply. After the out-of-network deductible is met, the plan reimburses a percentage of the insurer’s “allowed amount” — which is far below our actual fee. The patient pays the difference.

- POS plans: Sit between HMO and PPO. Usually require a referral and pay less out-of-network than a true PPO.

- Self-funded employer plans (ERISA): Highly variable. Some pay overseas mental health benefits as a deliberate inclusion for international staff; most don’t.

Two practical steps: (1) get the plan’s full Summary of Benefits and Coverage and read the out-of-network section, (2) call the behavioural-health number on your card and ask specifically about “non-network international inpatient substance use treatment” — and ask for the call reference.

Not sure what your policy actually covers? Send us a copy of your policy schedule — we’ll help you work out what to ask your insurer and what documentation we can provide.

Are Expat International Plans the Best Bet?

Yes — international expat plans designed for people living abroad are usually the most likely to cover residential addiction treatment in Thailand, because the entire point of the plan is to cover medical care wherever you happen to live. Cigna Global, William Russell, AXA Global Healthcare, and Allianz Care all offer some level of inpatient mental health cover, but addiction-specific benefits often sit behind a higher tier or optional module.

Important distinctions among the main expat insurers:

- Cigna Global: Inpatient mental health is standard on Silver, Gold, and Platinum tiers. Addiction treatment specifics depend on the plan version and any underwriting exclusions added at application (Cigna Global, 2026).

- William Russell: Gold and Silver plans cover inpatient mental health treatment. Addiction is sometimes treated as a separate benefit category — check the certificate of insurance.

- Allianz Care: The base plan does not cover drug or alcohol addiction treatment. Higher tiers and corporate plans sometimes do, but only when explicitly stated.

- AXA Global Healthcare: Inpatient psychiatric cover is standard on most international policies; addiction is usually a benefit with its own annual limit.

The pattern across all four: addiction is a “second-class” benefit hidden inside the broader mental health module. Always read the schedule of benefits before assuming you’re covered.

We had a client recently who’d been told by his expat insurer that his policy covered “mental health inpatient treatment” up to a generous annual limit. He arrived expecting reimbursement. When we helped him submit the claim, the insurer’s response was that addiction sat under a different sub-limit — a fraction of the headline figure. The lesson we tell every client now: read the schedule of benefits line by line, ask specifically about substance use disorder, and get every promise in writing before you fly.

Alastair MordeyProgramme Director, One Step Rehab

How Do You Actually Use Insurance to Pay for Rehab Abroad?

The difference between getting reimbursed and getting denied usually comes down to three things: documenting medical necessity before you travel, requesting pre-authorisation in writing, and submitting a clean claim pack afterwards. Skip any of those steps and you’re starting from a much harder position.

The practical workflow that works:

- Get a medical-necessity letter from a treating clinician. A GP, psychiatrist, or addiction physician at home writes a letter explaining your diagnosis (ICD-11 or DSM-5 code), why outpatient treatment isn’t enough, and why residential care is clinically indicated. This is the single most important document.

- Call the insurer’s medical pre-authorisation line. Not the general customer service number. Explain that you intend to undergo residential addiction treatment outside your home country. Ask for written pre-approval and a claim reference number.

- Get the rehab’s documentation pack. Admission letter, treatment plan, clinical formulation. We send all of this to clients on request before they arrive.

- Keep weekly clinical notes and a discharge summary. The insurer wants evidence the treatment actually happened and that progress was clinically tracked.

- Submit an itemised invoice and proof of payment. Most insurers want a receipt showing the fee was paid, not just billed.

Reimbursement is then a matter of weeks (best case) to months (most cases) of correspondence. Some insurers reject the first claim regardless and require you to appeal. That’s frustrating, but not unusual — the same pattern shows up in US domestic claims, where prior authorisation and medical-necessity denials are some of the most common reasons insurers refuse residential inpatient substance use disorder treatment (Dickson-Gomez et al., Drug Alcohol Depend Rep, 2022).

What Does One Step Rehab Actually Do With Insurance?

One Step Rehab is private-pay. We do not direct-bill insurers and we are not in-network with any UK, US, Australian, or European insurance scheme. What we do provide is a complete documentation pack so clients can submit reimbursement claims to their own insurer — admission letter, clinical formulation, weekly clinical notes, itemised invoice, and a discharge summary on completion.

The honest position:

- Fee: Approximately ฿280,000/month (~$8,500 USD). See our pricing page for what’s included and what isn’t.

- Payment: Up front, by bank transfer, before admission. We do not invoice insurers, and we do not extend credit while a claim is in progress.

- Documentation we provide: Admission letter on letterhead, clinical formulation, weekly progress notes, itemised invoice, and a written discharge summary. We can also write to a treating clinician at home if continuity-of-care documentation is needed.

- What we don’t do: Direct billing, network agreements, or pre-authorisation phone calls with insurers on a client’s behalf. The conversation with your insurer is yours to have — we’ll give you the paperwork to support it.

This is the standard model for residential rehabs in Thailand, including the other Chiang Mai operators. None of us are in-network with Western insurers — the regulatory and accreditation hurdles to becoming a contracted provider for BUPA or Aetna would push our fee well past the ฿280,000/month mark, which would defeat the point of why people travel here. For more on the trade-offs of choosing Chiang Mai over other Thai cities, see why we recommend Chiang Mai over Bangkok or Phuket, and for the broader case for treatment in Thailand, our primer on choosing Thailand for addiction treatment.

Medication prescribed by the doctor during your stay is billed separately, alongside other excluded items like flights, visas, and personal items. That’s standard across the industry but worth knowing before you set a budget.

What Should I Know If I’m Coming From a Specific Country?

Coverage varies enough by country that the same insurer can pay one client and refuse another based on policy version. Below is the rough lay of the land for the countries most of our clients come from, with the caveat that you must check your specific policy schedule.

| Country | What’s possible | What to ask |

|---|---|---|

| United Kingdom | Private medical (BUPA, AXA PPP, Aviva, Vitality) may pay limited day allowance for UK clinics; overseas rare | Day allowance for addiction; whether overseas is covered with prior approval |

| Netherlands | Zorgverzekering can reimburse a fraction under non-contracted GGZ pathway with GP referral | Verwijsbrief from huisarts; ongecontracteerde zorg rate; whether you have a naturapolis or restitutiepolis |

| Australia | Private hospital cover rarely pays overseas; early-release super on compassionate grounds is the more common route | ATO compassionate-release eligibility; specialist letter for medical necessity |

| Ireland | VHI, Laya, Irish Life Health follow a similar pattern to UK — domestic clinics only, with limited mental health benefits | Whether mental health module includes substance use; overseas treatment provisions |

| United States | PPO out-of-network may reimburse partial; HMO/EPO/ACA marketplace generally no | Out-of-network deductible, “allowed amount” for SUD inpatient, whether the plan has any international benefit |

| Regional Asia expats | Cigna Global, William Russell, AXA Global, BUPA Global often the most workable | Whether addiction sits inside the mental health module or has its own (smaller) limit |

What’s the Practical Reality of Funding Rehab Abroad?

Most people who come here pay up front and treat any reimbursement as a refund, not a budget line. Build your funding plan assuming zero insurance contribution. If a claim succeeds, the money goes back into your aftercare budget or your post-treatment savings. If it doesn’t, you haven’t built a treatment plan that depends on money you might never see.

A practical funding stack we see work for clients:

- Liquid savings or a structured family loan as the primary source

- Insurance reimbursement as a recovery line item, processed after discharge, with no expectation of timing

- For Australians: early-release super on compassionate grounds, applied for before travel

- For UK clients with a strong domestic insurance benefit: sometimes a hybrid plan — use the UK insurer-funded days for a stabilisation stay, then transfer to overseas residential treatment for the longer therapeutic phase

The clients who get the worst experience are those who arrive expecting an insurance company to retroactively pay for treatment they didn’t pre-authorise. Insurers are well-practised at finding reasons to decline retrospective claims for “elective” overseas care. The clients who get the best experience are those who walk in with a paid-up plan, complete documentation, and the expectation that any reimbursement is gravy.

Frequently Asked Questions

Practical questions about using insurance for rehab abroad.

Almost never. Travel insurance covers emergency, unplanned medical care during a trip. Residential rehab is treated as planned, elective care for a pre-existing condition — both standard exclusions on travel policies. Even if a substance-related emergency occurred abroad, the insurer would pay for the acute hospital stay, not transfer to a residential programme.

You can submit a claim retrospectively, but the success rate is far lower than for pre-authorised treatment. Without prior approval, insurers commonly reject the claim outright on medical-necessity grounds. If pre-authorisation isn’t realistic, get the medical-necessity letter from a treating clinician anyway — it’s the strongest support for a retrospective appeal.

An admission letter on letterhead, a clinical formulation written by the treating team, weekly clinical progress notes, an itemised invoice with proof of payment, and a written discharge summary on completion. We can also write directly to a treating clinician at home if continuity-of-care documentation is requested.

It depends on the insurer’s network rules. Expat international insurers (Cigna Global, William Russell, AXA Global) treat licensed Thai facilities as eligible providers in many cases. Domestic UK, US, and Australian insurers more often require a contracted or in-network provider, which rules out most overseas rehabs.

No. The Mental Health Parity and Addiction Equity Act requires substance use benefits to be no more restrictive than medical benefits within the plan’s existing coverage rules. If the plan doesn’t cover overseas medical care, parity doesn’t force it to cover overseas substance use treatment either. Parity equalises benefits inside the network, not outside it.

Rarely fully. The Dutch basisverzekering can reimburse part of GGZ overseas care under specific conditions, but the rate is typically 50% to 80% of the NZa maximum tariff under non-contracted rules. A restitutiepolis pays more than a naturapolis. A verwijsbrief from your huisarts is essential to support the claim.

No. Build the budget assuming zero reimbursement. If the claim succeeds, the refund frees up money for aftercare, family travel, or post-discharge living costs. If it fails, your treatment plan isn’t compromised. Budgeting on the assumption of reimbursement is the single most common funding mistake we see.

Written by

Alastair Mordey

Alastair Mordey is one of the pioneers of drug and alcohol treatment globally and specifically in Asia. He has been an addiction’s professional for twenty years. He started his career as an expert in substance abuse w...

Learn more about Alastair

Medically reviewed by

Dr. Worapakthorn Kongpesalaphun

Consultant Psychiatrist · Thai Licensed Medical Doctor · Residency in Psychiatry, Somdet Chaopraya Institute · Doctor of Medicine, Rangsit University

Dr. Worapakthorn Kongpesalaphun is a Thai Licensed Medical Doctor and Expert in Preventive Medicine (Community Mental Health) with extensive experience in addiction treatment and public health management. He holds multip...

Learn more about Dr. Worapakthorn